How I Tamed Medical Bills Without Breaking the Bank

Facing medical expenses can feel like staring down a financial cliff. I’ve been there—stressed, confused, and scrambling to cover costs that came out of nowhere. It hit me hard when a surprise health issue turned into a mountain of bills. But over time, I learned smart ways to plan ahead, protect my savings, and handle healthcare costs without panic. This is how I rebuilt my financial calm—one practical move at a time.

The Wake-Up Call: When Health Costs Hit Home

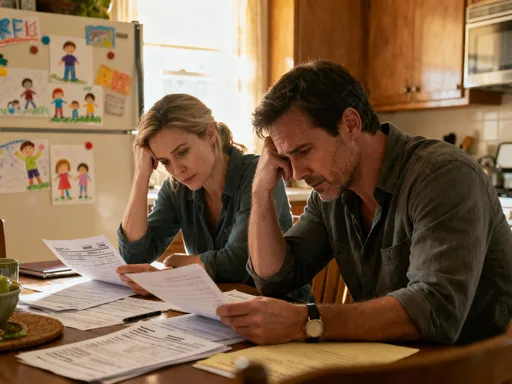

It started with a sharp pain in my side and a quick trip to the emergency room. What I thought would be a routine check-up turned into an urgent diagnosis: kidney stones requiring immediate treatment. Within days, I was navigating a maze of specialists, imaging scans, and follow-up care. The medical part was hard enough—but the bills that followed were even harder to swallow. The first statement arrived in the mail—$4,800 for services I assumed my insurance would cover. I stared at the numbers, heart sinking. I had insurance, yes, but not the kind that shielded me completely. Deductibles, co-pays, and out-of-network charges added up fast, turning what should have been manageable into a financial crisis.

This experience was not unique. Millions of Americans face similar shocks every year. According to data from the Kaiser Family Foundation, nearly half of U.S. adults report difficulty paying medical bills, with many forced to cut back on essentials like food and housing. Even those with insurance are vulnerable. A single unexpected procedure, hospital stay, or chronic condition can quickly exceed annual deductibles and exhaust savings. The emotional toll is just as heavy—stress, sleepless nights, and a constant sense of insecurity. For many women in their 30s to 50s, who often manage both household finances and caregiving, the pressure is especially intense.

What became clear to me was this: having insurance is only the first step. It is not a complete financial safety net. Gaps exist—sometimes wide ones—and without preparation, those gaps can swallow a budget whole. The wake-up call wasn’t just about my health. It was about financial resilience. I realized I needed a new approach—one that combined smart planning, proactive habits, and practical tools to prevent future crises. This journey began not with a windfall or a miracle, but with small, deliberate choices that added up to real control.

Building Your Financial Safety Net: More Than Just Insurance

Insurance is essential, but it should never be mistaken for a complete solution. Most health plans require policyholders to pay deductibles before full coverage kicks in. Even after meeting those thresholds, co-insurance and co-pays can accumulate quickly. Some services—like dental, vision, or alternative therapies—are often excluded entirely. For families managing multiple prescriptions or ongoing treatments, these uncovered costs can become a hidden burden. Relying solely on insurance is like building a house on sand; it may stand for a while, but one strong storm can bring it down.

A true financial safety net goes beyond the policy document. It includes a dedicated emergency fund specifically for health-related expenses. Financial experts often recommend saving three to six months’ worth of living expenses, but for medical preparedness, an additional buffer makes sense. A target of $1,000 to $5,000 in a readily accessible account can cover unexpected co-pays, diagnostics, or prescriptions before insurance fully engages. This fund isn’t meant for vacations or car repairs—it’s reserved for health surprises, large or small.

Where to keep this money matters. A high-yield savings account offers modest growth while maintaining liquidity. Unlike investments, which can fluctuate in value, cash in a savings account is stable and available when needed. One mother of two shared how her $2,500 medical reserve covered her daughter’s emergency dental procedure without touching her credit card. Another woman used her fund to pay for physical therapy after a fall, avoiding a loan. These aren’t extravagant sums, but they provided critical breathing room. The key is consistency—setting aside even $50 a month builds protection over time.

Equally important is knowing how to access the fund without guilt. Some people hesitate to use savings, fearing they’ll never rebuild the balance. But emergency funds exist for emergencies. Withdrawing for a legitimate health cost isn’t failure—it’s responsible planning in action. Replenishing the fund once the crisis passes closes the loop and strengthens long-term discipline. The goal isn’t perfection; it’s preparedness. When the next health issue arises—and for most, it’s not a matter of if, but when—that cushion can mean the difference between stress and stability.

Smart Use of Health Savings Accounts (HSAs) and FSAs

Among the most powerful tools for managing medical costs are Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). Both offer tax advantages, but they work differently and serve distinct purposes. An HSA is available to those enrolled in a high-deductible health plan (HDHP). It allows pre-tax contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses—making it a rare triple tax-advantaged account. Unlike FSAs, HSA funds roll over year after year, never expire, and can even be invested for long-term growth. This makes HSAs not just a spending tool, but a strategic asset in a financial plan.

FSAs, on the other hand, are typically offered through employers and allow pre-tax contributions for medical, dental, and vision costs. The major drawback is the “use-it-or-lose-it” rule—any unused balance at year-end is forfeited, though some plans offer a small carryover or grace period. Because of this, FSA spending requires more careful planning. Still, for predictable expenses like prescription co-pays, contact lenses, or annual screenings, an FSA can significantly reduce out-of-pocket costs over the year.

Maximizing these accounts starts with enrollment. Too many eligible individuals skip signing up during open enrollment, missing out on tax savings. For 2024, the IRS allows HSA contributions of up to $4,150 for individuals and $8,300 for families, with an additional $1,000 catch-up for those 55 and older. Even contributing half that amount can yield meaningful benefits. One woman in her 40s contributed $200 monthly to her HSA, building over $5,000 in five years. When she needed minor surgery, she paid the entire bill from her account—no out-of-pocket cost, no debt.

The real power of an HSA emerges over time. After age 65, funds can be withdrawn for any purpose without penalty (though non-medical withdrawals are taxed as income). This dual-use feature makes HSAs a stealth retirement tool. Many financial advisors now recommend treating HSAs like supplemental retirement accounts—paying current medical costs from savings and letting the HSA grow tax-free for future use. It’s a strategy that requires discipline, but the payoff is substantial. By viewing these accounts as long-term assets, not just short-term expense tools, individuals gain greater control over both health and wealth.

Navigating Bills and Negotiating Like a Pro

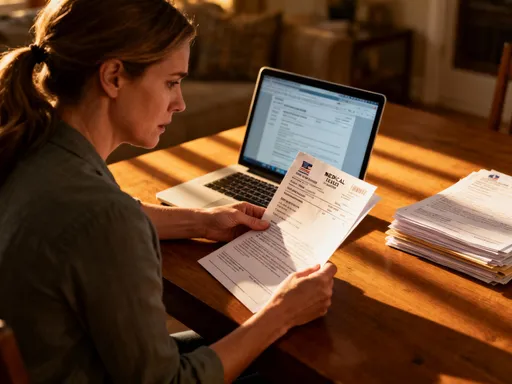

One of the most unsettling aspects of medical care is the billing process. Charges are often unclear, codes are confusing, and itemized statements can look like foreign languages. It’s not uncommon for errors to appear—duplicate charges, incorrect procedure codes, or services never rendered. A study by the Medical Billing Advocates of America found that over 80% of medical bills contain mistakes. Yet, most patients pay without questioning, assuming the numbers are final. The truth is, bills are not set in stone. They are negotiable—and speaking up can lead to significant savings.

The first step is to request an itemized bill. This detailed breakdown lists every service, medication, and facility fee. Review it carefully. Look for charges that seem excessive—like a $100 fee for a basic bandage or $300 for a routine blood draw. Compare the services listed with your memory of the visit. If something doesn’t match, note it. Errors are common, especially in emergency settings where documentation is rushed. One woman discovered she was billed for an MRI she never had—correcting it saved her $1,200.

Once the bill is reviewed, call the provider’s billing department. Be polite but firm. Ask for a detailed explanation of charges and express concern about accuracy. Many offices have financial counselors trained to assist patients. At this stage, you can request a discount—especially if paying in full. Hospitals and clinics often have sliding-scale programs or charity care policies for those with limited income. Even without qualifying for assistance, simply asking for a reduction can yield results. One patient reduced a $3,000 bill to $1,800 by requesting a cash-pay discount.

Payment plans are another option. Rather than maxing out a credit card, negotiate a no-interest installment agreement. Many providers offer 12 to 24 months of deferred payments with no fees. Some may require a small down payment, but the relief is immediate. The key is to act quickly—before the account goes to collections. Once a bill is overdue, options shrink and stress grows. By addressing charges early, staying organized, and advocating clearly, patients can turn overwhelming statements into manageable obligations. The lesson is simple: silence costs money. Speaking up saves it.

Planning Ahead: Forecasting and Preventing Future Shocks

Reactive financial management leads to stress. Proactive planning leads to peace. One of the most effective ways to reduce medical costs is to prevent them before they occur. Preventive care—annual check-ups, screenings, vaccinations, and early interventions—can catch health issues when they are easier and less expensive to treat. A mammogram that detects early-stage breast cancer, for example, can prevent far more costly treatments later. Yet, many women delay or skip these services due to cost concerns, time constraints, or lack of awareness.

Most insurance plans cover preventive services at no cost to the patient, thanks to the Affordable Care Act. This includes blood pressure checks, cholesterol tests, diabetes screenings, and colonoscopies after age 45. Taking full advantage of these benefits is a smart financial move. It’s like getting free maintenance for your body—something no one would skip on a car. Scheduling annual visits and staying up to date on recommendations reduces the risk of expensive emergencies down the road.

Another key step is forecasting potential costs based on personal and family health history. If heart disease runs in your family, regular cardiac screenings may be wise. If you have children with allergies, having an EpiPen on hand—and knowing how to use insurance to cover it—is part of preparedness. Lifestyle factors matter too. Managing weight, staying active, and avoiding smoking all lower the risk of chronic conditions like diabetes and hypertension, which drive long-term medical spending.

Building a personal health forecast into your budget makes sense. Set aside a small amount each month—$25 to $100—based on your risk profile. Use it for co-pays, over-the-counter medications, or wellness programs. This proactive allocation turns unpredictable costs into planned expenses. One woman in her 50s began budgeting $75 monthly for health, covering everything from supplements to therapy sessions. Over time, she avoided debt and felt more in control. Prevention isn’t just about health—it’s about financial security. The earlier you start, the greater the protection.

Investment Moves That Support Health Financially

While emergency funds and HSAs handle immediate needs, long-term investments provide deeper financial resilience. The goal isn’t to chase high returns, but to build a diversified portfolio that balances growth with safety. When medical issues arise later in life—such as joint replacements, vision surgery, or chronic disease management—having accessible, stable assets can prevent forced withdrawals from retirement accounts or reliance on debt.

Low-risk, liquid investments are ideal for health-related goals. Short-term bond funds, money market accounts, and dividend-paying stocks offer modest returns with less volatility than growth stocks. These assets can be tapped if needed without selling during market downturns. For those in their 40s and 50s, allocating a portion of the portfolio to such instruments creates a bridge between emergency savings and long-term retirement funds.

Diversification is key. Spreading investments across asset classes—stocks, bonds, real estate, and cash equivalents—reduces risk. A balanced mix grows steadily over time, helping offset inflation and rising healthcare costs. According to Fidelity, the average 65-year-old couple retiring today may need over $300,000 to cover medical expenses in retirement, not including long-term care. Planning for this reality requires disciplined saving and smart investing long before retirement age.

Automating contributions to investment accounts ensures consistency. Even $100 a month invested in a low-cost index fund can grow significantly over 10 to 20 years. The power of compound interest means early action yields outsized benefits. One woman began investing $150 monthly at age 42. By 60, her account had grown to over $50,000—enough to cover multiple medical procedures without debt. The lesson is clear: investing isn’t just for retirement. It’s a form of health protection. Financial strength supports physical well-being by removing the fear of cost as a barrier to care.

Creating a Realistic, Sustainable Financial Health Plan

All these strategies—emergency savings, HSAs, bill negotiation, prevention, and investing—come together in a single, personalized financial health plan. The first step is assessment. Take stock of your current situation: insurance coverage, savings, debt, and health history. Identify gaps. Are you underinsured? Do you lack a medical reserve? Is your HSA underfunded? Honest evaluation reveals where action is needed.

Next, set specific, achievable goals. Maybe it’s building a $3,000 emergency fund in 18 months, maxing out your HSA contribution, or scheduling overdue screenings. Break each goal into monthly actions. Automate savings if possible. Track progress regularly. Use a simple spreadsheet or budgeting app to stay on course. Small, consistent steps build momentum and confidence.

Finally, review and adjust. Life changes—jobs, family size, health status—and your plan should too. Annual check-ins ensure alignment with current needs. Celebrate progress, even if it’s incremental. Paying off a medical bill, catching a billing error, or completing a preventive test are all wins. Financial health isn’t about perfection. It’s about progress, resilience, and peace of mind.

Managing medical costs doesn’t require a finance degree or a six-figure income. It requires awareness, intention, and action. By taking control step by step, you protect not just your wallet, but your well-being. True security comes not from avoiding illness, but from knowing you can handle it—without losing sleep or savings. That peace is worth more than any dollar amount. And it’s within reach, one smart choice at a time.